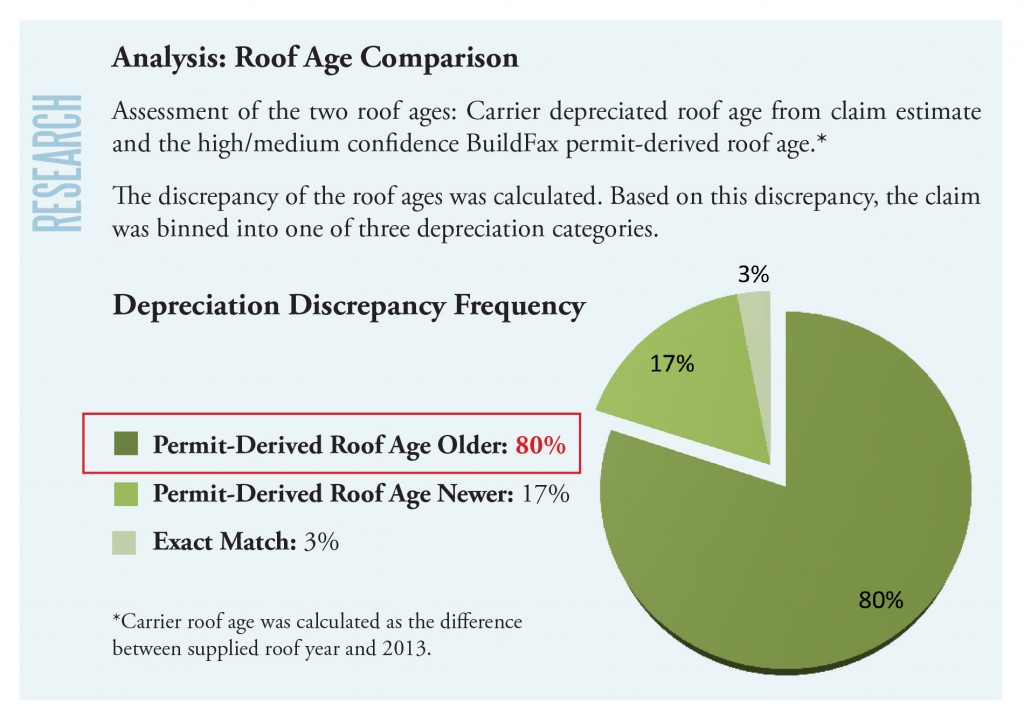

Roof Depreciation Life

Part Three The Value Of Accurate Roof Age In Claims

Roof Insurance Claim Process Questions Bob Behrends Roofing Gutters

Calculating Roof Depreciation In An Insurance Claim The Voss Law Firm P C

What Is The Depreciation Of The Roof On A Commercial Building

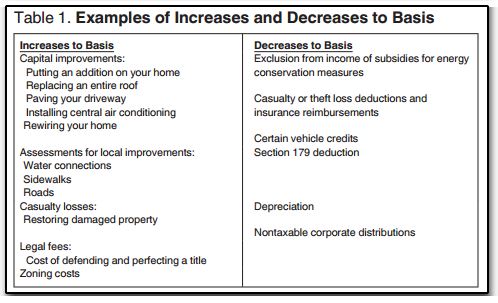

12762 Increasing Basis On An Asset Being Depreciated

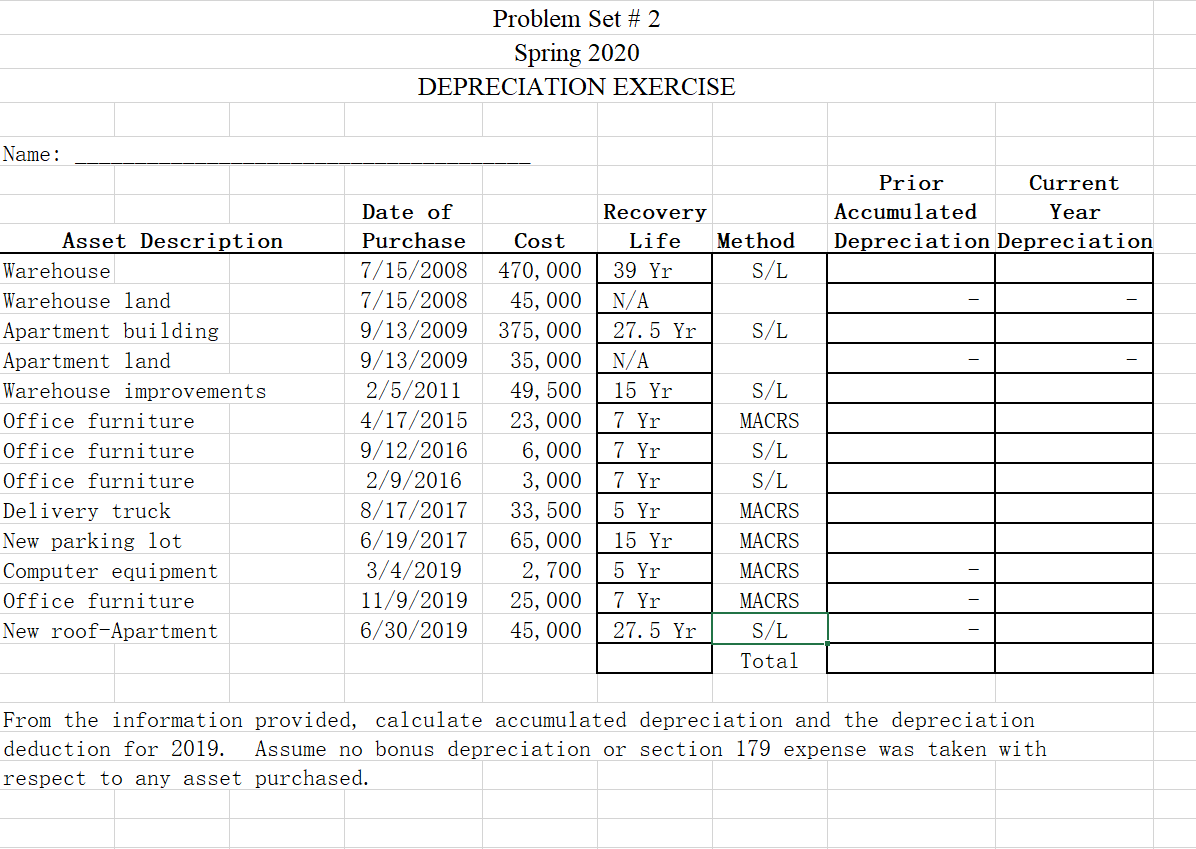

Problem Set 2 Spring 2020 Depreciation Exercise Chegg Com

10 000 for the first year 16 000 for the second year.

Roof depreciation life.

Rcv Vs Acv Whats The Difference A Young Insurance Agency Inc

How Rental Property Depreciation Works The Benefits To You

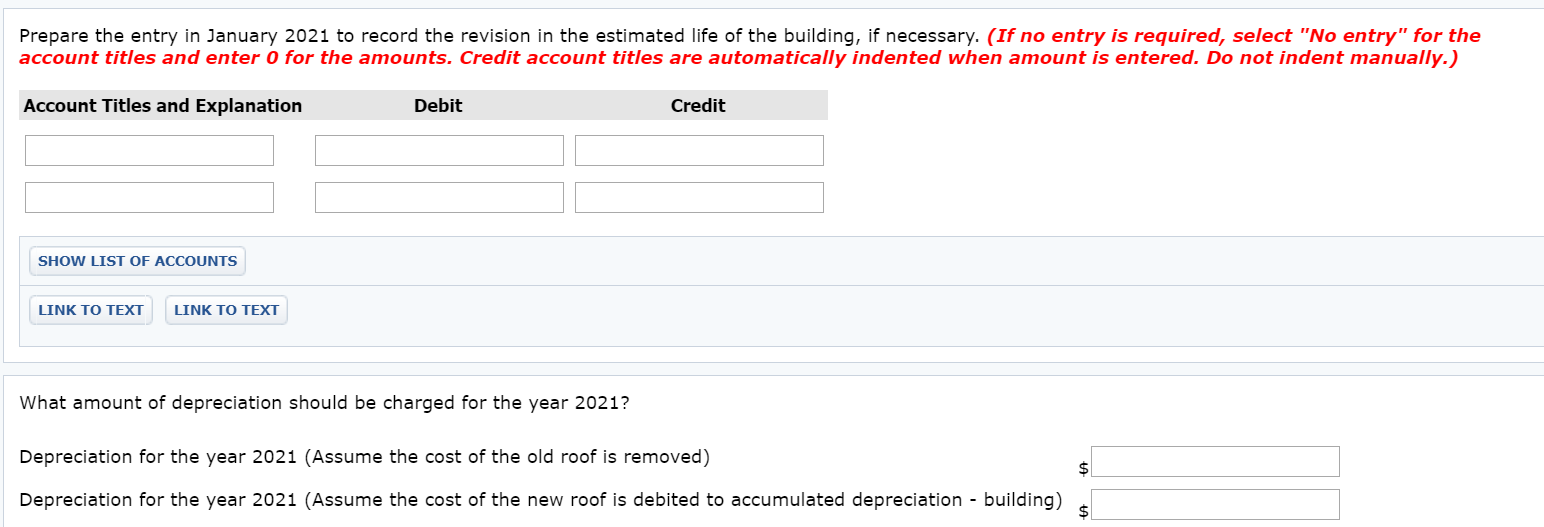

Solved Exercise 11 13 Concord Company Constructed A Build Chegg Com

How To Understand Depreciation On Your Roof Insurance Claim

Chapter 14 Cost Approach Cost Approach The Cost Approach Is Most Useful When Property Is Unique Property Is Reasonably New And The Improvements Ppt Download

How Does Recoverable Depreciation Impact My Home Insurance Claim Valuepenguin Insurance Deductible Home Insurance Insurance Marketing

Homeowners Insurance 101 Roof Age Matters At Claim Time

Rental Property Depreciation Reducing Your Tax Burden 37parallel Com

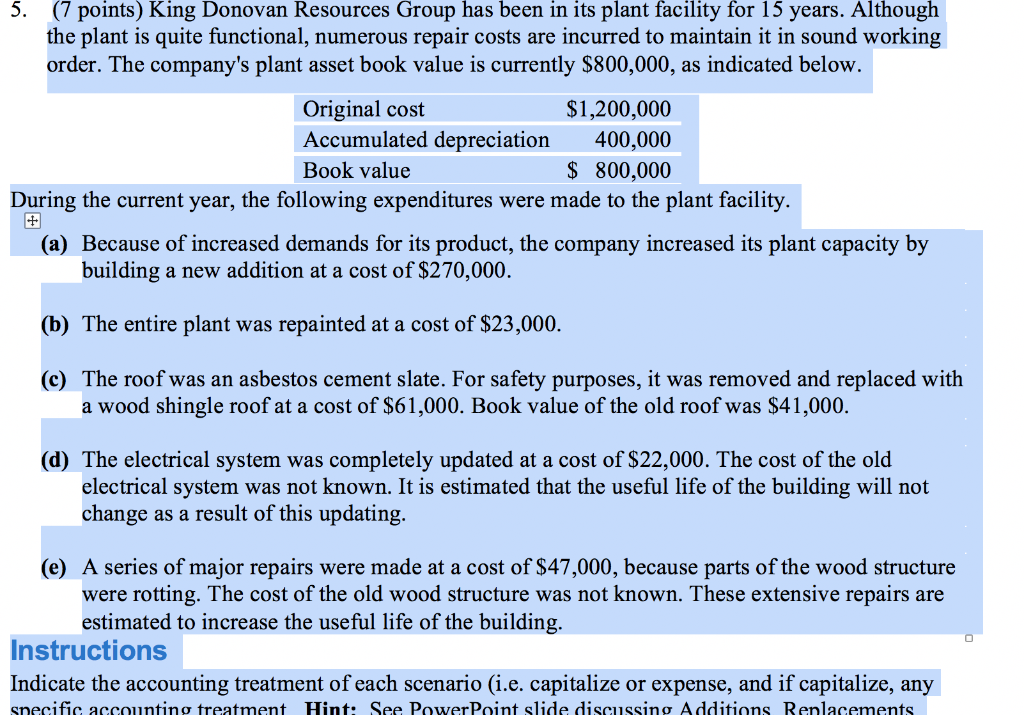

Solved 7 Points King Donovan Resources Group Has Been I Chegg Com

Can I Make Money Off My Insurance Roofing Claim Slade Roofing

My Roof Needs To Last How Long

Overview Of The Cost Approach Final Reconciliation Ppt Download

Depreciating Labor Costs The Rough Notes Company Inc

Bonus Depreciation Kbkg

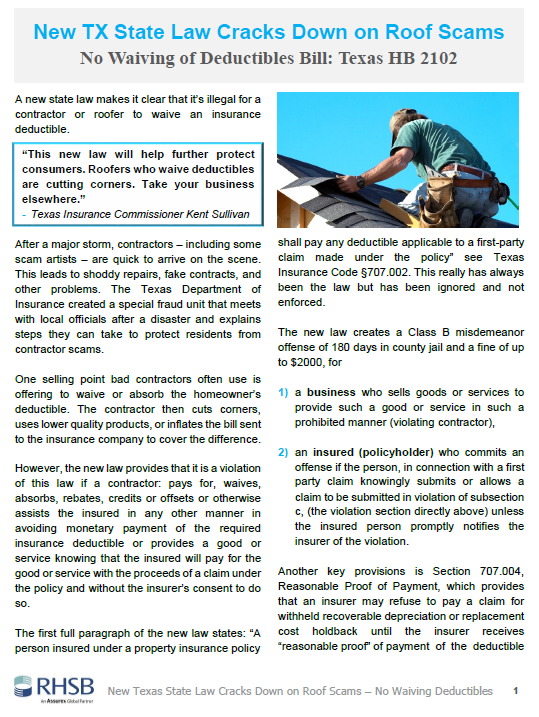

New Tx State Law Cracks Down On Roof Scams No Waiving Deductibles Rhsb

179 Tax Deduction For Commercial Roofing Projects Advanced Roofing Inc

Understanding Qualified Improvement Property Depreciation Changes Mlr

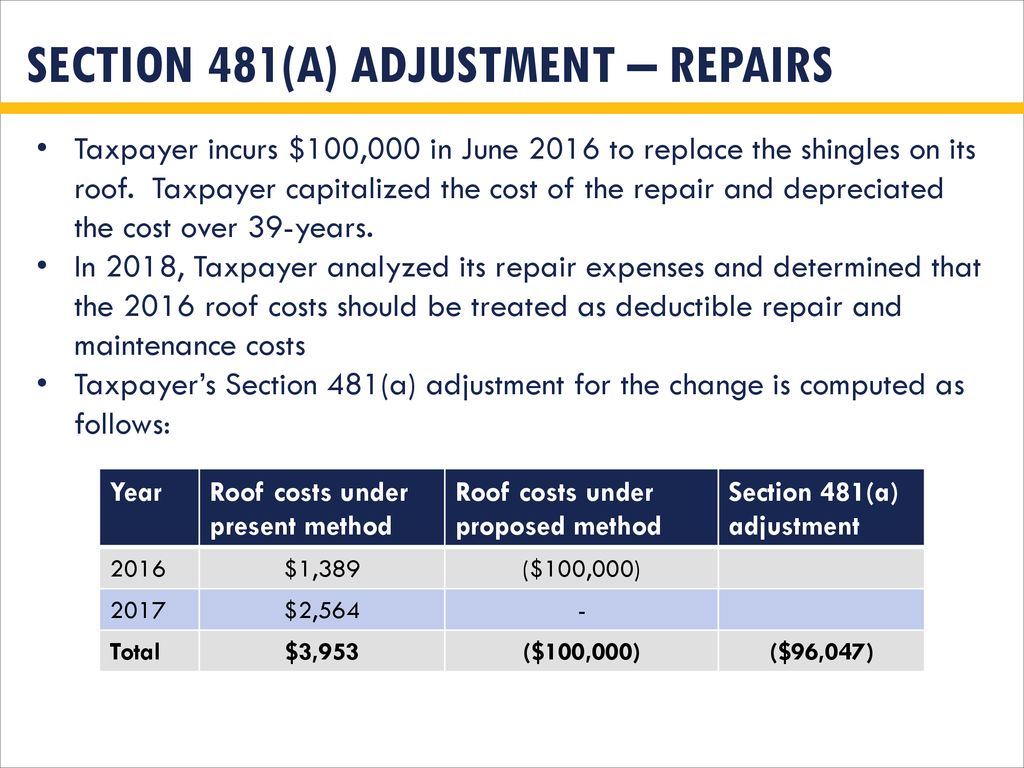

Accounting Method Changes Post Tax Reform Ppt Download

Section 179d Tax Deduction For Commercial Roof Replacements

Roof Insurance Claim Denied

Highland Commercial Roofing Trump Tax Code Effects On Roofing

4562 Half Year Mid Month And Mid Quarter Conventions 1120 1120s 4562

How Long Does A Roof Last Age Of Roof And Insurance Harry Levine

Actual Cash Value Is The Cost Of Labor Part Of Depreciation The Courts Are Divided Insurance And Reinsurance Disputes Blog

Irs Issues Guidance For Change To Real Property Depreciation Grant Thornton

Depreciation Recapture What Is It And How Can I Reduce It

Roof Insurance Acv Vs Replacement Cost Bankrate

Heatspring Magazine Finance 101 For Solar Pv Professionals

How Does Recoverable Depreciation Impact My Home Insurance Claim Valuepenguin

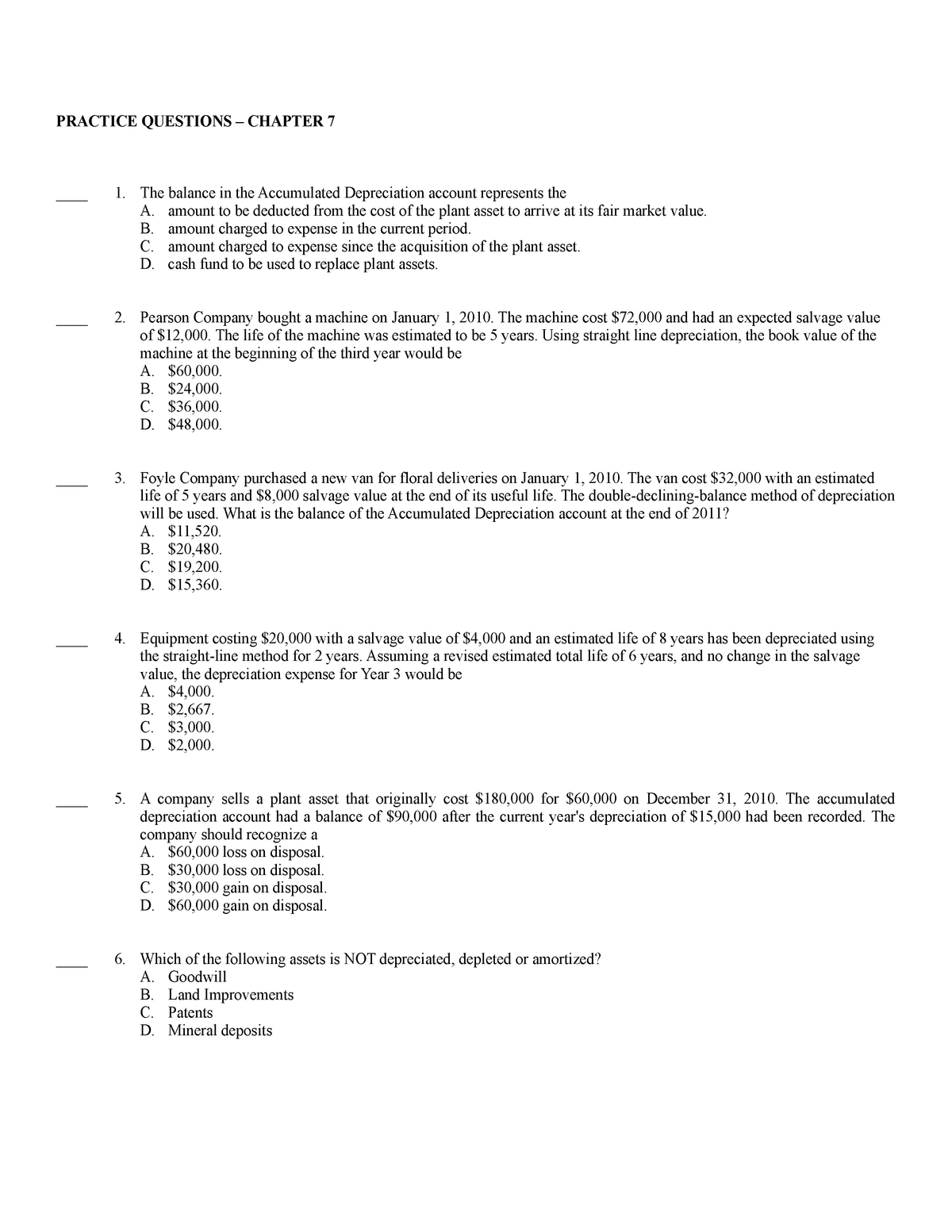

Acct 101 Chapter 7 Practice Questions 101 Smu Studocu

What Is Qualified Leasehold Improvement Property

Why Depreciation Matters For Rental Property Owners At Tax Time Stessa

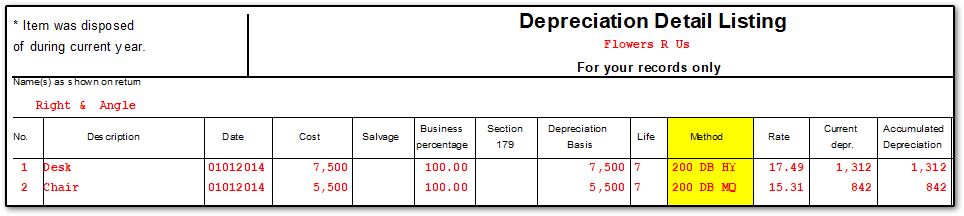

Streamline The Complicated Task Of Fixed Assets Depreciation Asset Panda

The Top 14 Rental Property Tax Deductions Investors Should Know

Replacing Your Roof With An Insurance Claim

What Recoverable Depreciation Means And How To Calculate It

Understanding Recoverable Depreciation In An Insurance Claim The Voss Law Firm P C

What Is Rental Property Depreciation And How Does It Work

Average Flat Roof Membrane Life Span Roofslope

Understanding Depreciation Recapture Taxes On Rental Property Rental Property Being A Landlord Military Housing

Depreciation Life On Permanent Houseboat Used As R Intuit Accountants Community

Cost Segregation Bonus Depreciation Simple Passive Cashflow

How The New Tax Law Affects Rental Real Estate Owners

Depreciable Life Life Expectancy For Rental Purchases

Source : pinterest.com